Monetary Growth and Inflation

Help Questions

AP Macroeconomics › Monetary Growth and Inflation

Based on the money supply growth shown, assume real GDP growth stays at 3% and velocity is stable in the long run. Which statement correctly distinguishes nominal from real outcomes in the long run?

Table: Long-Run Growth Rates (Economy E)

Variable | Growth rate

---|---:

Money supply | 9%

Real GDP | 3%

Inflation becomes unpredictable because stable real GDP growth implies unstable velocity in the long run.

The price level is unchanged because money growth affects only real variables in the long run.

Inflation falls because higher money growth permanently lowers the real interest rate in the long run.

Nominal variables, including the price level, grow faster while real GDP growth remains tied to real factors in the long run.

Real GDP growth rises to match money growth because more money directly increases productive capacity in the long run.

Explanation

Monetary growth measures how quickly the money supply is increasing, while inflation captures the rate at which prices are rising on average. Under long-run neutrality of money, alterations in money supply influence nominal outcomes like the price level but not real ones such as output growth. With the table showing 9% money growth and 3% real GDP growth, nominal variables accelerate (e.g., inflation ~6%) while real GDP remains anchored at 3%. A common error is assuming money growth boosts real GDP by creating resources, but money is just a veil over real exchanges in the long run. Use the strategy of subtracting real output growth from money growth to estimate inflation, distinguishing nominal from real effects as in choice A.

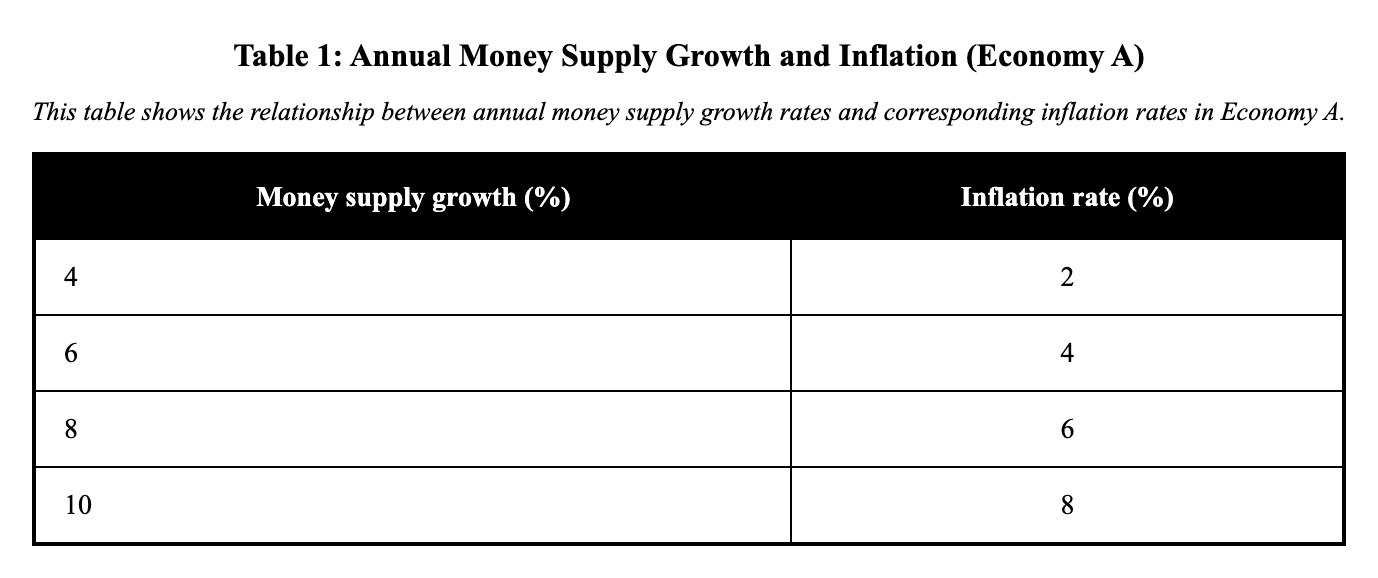

Based on the money supply growth shown in the table, assume real GDP grows at a stable 2% per year and velocity is stable in the long run. In the long run, what outcome is most consistent with the relationship between sustained money growth and inflation?

Table: Annual Money Supply Growth and Inflation (Economy A)

Money supply growth (%) | Inflation rate (%)

---|---

4 | 2

6 | 4

8 | 6

10 | 8

The sustained rise in money growth causes the price level to rise faster while real GDP growth remains at its long-run rate.

The sustained rise in money growth causes real GDP growth to rise persistently because more money creates more real resources.

The sustained rise in money growth causes the price level to fall as higher money growth reduces the overall cost of borrowing.

The sustained rise in money growth mainly changes velocity unpredictably, so inflation has no systematic long-run relationship to money growth.

The sustained rise in money growth causes real GDP growth to rise persistently while inflation stays near 2% per year.

Explanation

Monetary growth refers to the rate at which the money supply increases over time, while inflation is the sustained rise in the general price level, often measured as a percentage change. The long-run neutrality of money implies that changes in the money supply affect nominal variables like prices but do not alter real variables such as real GDP growth, which depends on factors like technology and labor. In this scenario, the table shows that as money supply growth rises from 4% to 10%, inflation increases proportionally from 2% to 8%, with real GDP growth stable at 2%, illustrating how excess money growth fuels inflation. A common misconception is that higher money growth can permanently boost real GDP, but this confuses nominal spending with real output, as money is neutral in the long run. To predict long-run inflation, compare money growth to real output growth: here, inflation approximates money growth minus 2%, matching the table's pattern and supporting choice A.

Based on the money supply growth shown, assume real GDP growth is stable at 4% per year and velocity is stable in the long run. Using the distinction between money growth and output growth, which statement best describes the long-run implication for inflation?

Table 5: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 12, Inflation 8

Year 2: Money growth 12, Inflation 8

Year 3: Money growth 12, Inflation 8

Inflation will be about 8% per year because sustained money growth exceeds long-run real GDP growth by about 8 percentage points.

Inflation will be about 12% per year because sustained money growth always equals inflation when velocity is stable.

Inflation will be unrelated to money growth because velocity becomes unstable whenever money growth is sustained.

The price level will remain stable because long-run money neutrality implies money growth has no effect on nominal variables.

Real GDP growth will increase toward 12% per year because sustained money growth raises productivity in the long run.

Explanation

Monetary growth describes the pace at which the money supply expands, while inflation is the continuous escalation of the general price level. According to long-run money neutrality, alterations in money supply impact nominal elements like prices but leave real factors, such as GDP growth, determined by non-monetary influences. With 12% money growth, 4% real GDP growth, and stable velocity, the scenario predicts 8% inflation, as reflected in the table, via the quantity equation's logic. One misconception is that high money growth inherently boosts long-run productivity and real output, but neutrality reveals it only inflates prices. A key strategy is to contrast money growth with real output growth; their difference offers a reliable inflation estimate under stable conditions.

Based on the money supply growth shown, assume potential real GDP is growing at a stable 2% per year and velocity is stable in the long run. Using long-run money neutrality and quantity theory intuition, which conclusion is most consistent with the data?

Table 4: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 4, Inflation 2

Year 2: Money growth 4, Inflation 2

Year 3: Money growth 4, Inflation 2

Inflation will be about 4% per year because money growth determines inflation one-for-one even when real GDP is growing.

The price level will fall because higher money growth raises real output more than nominal spending in the long run.

Real GDP growth will rise to about 4% per year because sustained money growth increases long-run aggregate supply.

Inflation will be about 2% per year because money growth exceeds long-run real GDP growth by about 2 percentage points.

Inflation cannot be linked to money growth because stable velocity implies inflation is determined only by real GDP growth.

Explanation

Monetary growth is the rate of increase in the money supply, and inflation measures the average rise in prices over time. Long-run neutrality of money implies that money supply adjustments affect nominal variables like the price level but not real ones like potential GDP growth. Given 4% money growth, 2% real GDP growth, and stable velocity, the data shows inflation at 2%, consistent with quantity theory where money growth minus output growth yields inflation. A common misconception is that money growth always equals inflation one-for-one, ignoring how real growth absorbs some monetary expansion without price hikes. To apply this broadly, subtract real output growth from money growth to predict inflation, highlighting the monetary roots of price changes.

Based on the money supply growth shown, assume long-run real GDP growth is stable at 2% and velocity is stable. Which statement best explains why higher sustained money growth is associated with higher long-run inflation?

Table: Sustained Growth Rates (Economy C)

| Period | Money supply growth (%) | Real GDP growth (%) |

|---|---|---|

| 1 | 3 | 2 |

| 2 | 7 | 2 |

| 3 | 11 | 2 |

With stable velocity and stable real output growth, faster money growth lowers the price level by increasing the supply of goods and services.

With stable velocity and stable real output growth, faster money growth translates into faster growth of nominal spending and the price level.

With stable velocity and stable real output growth, faster money growth affects only real variables, so the price level is unchanged in the long run.

With stable velocity and stable real output growth, faster money growth permanently raises real GDP by shifting LRAS to the right.

With stable velocity and stable real output growth, faster money growth reduces inflation because nominal wages adjust downward in the long run.

Explanation

Monetary growth denotes the expansion rate of the money supply, whereas inflation is the persistent increase in the price level, eroding purchasing power. The principle of long-run neutrality of money states that monetary changes impact nominal aspects like inflation but not real ones like GDP growth over time. In the given table, periods with higher money growth (3% to 11%) and stable 2% real GDP growth result in higher inflation, as nominal spending grows faster than real output. A frequent misconception is that more money directly creates more real resources, leading to higher GDP, but this overlooks money's neutrality and the role of real factors in output. For a transferable approach, always compare money growth to real output growth to gauge inflation pressure, explaining why faster money growth drives price increases in choice A.

Based on the money supply growth shown, assume real GDP growth is stable at 2% per year and velocity is stable in the long run. If money supply growth increases permanently from 4% to 9%, which long-run change in inflation is most consistent with the data and the idea that inflation is a monetary phenomenon?

Table 9: Money Supply Growth and Inflation (Percent per Year)

Years 1–2: Money growth 4, Inflation 2

Years 3–4: Money growth 9, Inflation 7

Inflation rises in the long run because higher sustained money growth increases the growth rate of the price level when real GDP growth is stable.

Inflation falls in the long run because higher sustained money growth increases long-run real GDP growth and lowers prices through higher output.

Inflation becomes unrelated to money growth because stable velocity implies the central bank cannot influence nominal variables in the long run.

Inflation is unchanged in the long run because long-run money neutrality implies money growth has no effect on the price level.

Inflation rises in the long run because higher money growth directly increases long-run real GDP, which pushes up prices through higher demand.

Explanation

Monetary growth is the expansion rate of the money supply, whereas inflation measures sustained price increases. Long-run neutrality of money implies that money impacts nominal factors like inflation rates but not real growth trajectories. Shifting from 4% to 9% money growth with 2% real GDP and stable velocity raises inflation from 2% to 7%, as data indicates, because higher money growth accelerates price level changes. A misconception is that more money growth lowers inflation via higher output, but neutrality confirms real output stability, leading to higher inflation. Strategically, compare money growth to real output growth before and after changes to predict inflation shifts, emphasizing monetary causes.

Based on the money supply growth shown, assume real GDP grows at a stable 2% per year and velocity is stable in the long run. Using long-run neutrality of money, which statement correctly distinguishes nominal from real effects of sustained money growth?

Table 7: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 7, Inflation 5

Year 2: Money growth 7, Inflation 5

Year 3: Money growth 7, Inflation 5

Sustained money growth mainly stabilizes inflation over time, while long-run real GDP growth rises because nominal GDP is higher.

Sustained money growth mainly reduces long-run real GDP growth over time, while the price level is unchanged due to neutrality.

Sustained money growth mainly raises long-run real GDP growth over time, while the price level remains determined by real factors.

Sustained money growth mainly lowers the price level over time, while long-run real GDP growth rises due to higher real balances.

Sustained money growth mainly raises the price level over time, while long-run real GDP growth remains determined by real factors.

Explanation

Monetary growth is the rate of money supply expansion, while inflation tracks the upward trend in average prices. The long-run neutrality of money means monetary policy influences nominal outcomes but not real economic growth, which depends on real determinants. For 7% money growth and 2% real GDP growth with stable velocity, inflation at 5% distinguishes nominal effects (rising prices) from unchanged real growth, as per the data. A common misconception is that money growth enhances real GDP by increasing real balances, but neutrality shows it only scales nominal variables. To generalize, deduct real output growth from money growth to assess inflation potential, aiding in separating monetary from real impacts.

Based on the money supply growth shown, assume real GDP grows at a stable 3% per year and velocity is stable in the long run. Using the long-run distinction between money growth and output growth, which outcome is most consistent with sustained 8% money growth?

Table 2: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 8, Inflation 5

Year 2: Money growth 8, Inflation 5

Year 3: Money growth 8, Inflation 5

The price level will remain constant because long-run money neutrality implies money growth has no effect on nominal variables.

Inflation will be about 5% per year because money growth persistently exceeds real GDP growth by about 5 percentage points.

Inflation will be unpredictable because stable velocity implies money growth affects only real GDP, not the price level, in the long run.

Real GDP growth will be about 8% per year because higher money growth raises long-run aggregate supply by increasing investment.

Inflation will be about 3% per year because real GDP growth determines inflation when velocity is stable in the long run.

Explanation

Monetary growth is the percentage increase in the money supply, and inflation represents the ongoing rise in average prices across the economy. Long-run money neutrality means that while money supply changes impact nominal outcomes like the price level, they leave real economic variables, such as real GDP growth, unaffected in the long term. Here, with sustained 8% money growth and 3% real GDP growth under stable velocity, the quantity theory suggests inflation will hover around 5%, as the table indicates, because excess money chases the same real output. One misconception is believing higher money growth permanently elevates real GDP by stimulating investment, but neutrality clarifies that real growth stems from real factors, not monetary ones. A useful strategy is to subtract real output growth from money growth to estimate long-run inflation, providing a clear gauge of monetary pressure on prices.

Based on the money supply growth shown, assume potential real GDP grows at a stable 3% per year and velocity is stable in the long run. Which statement best summarizes the long-run implication of sustained money growth for nominal versus real variables?

Table 10: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 3, Inflation 0

Year 2: Money growth 3, Inflation 0

Year 3: Money growth 3, Inflation 0

Sustained money growth lowers the price level over time because higher money growth increases the value of money in the long run.

Sustained money growth can raise long-run real GDP growth over time, but the price level is determined by real factors and stays stable.

Sustained money growth can raise nominal variables like the price level over time, but long-run real GDP growth is determined by real factors.

Sustained money growth raises long-run real GDP growth over time, and inflation stays at zero because output growth absorbs all money growth.

Sustained money growth has no effect on nominal variables over time because long-run money neutrality applies to the price level as well.

Explanation

Monetary growth denotes the money supply's growth rate, and inflation is the rate of general price escalation. Long-run money neutrality means money affects nominal variables, such as the price level, but real GDP growth is shaped by real forces like productivity. Here, 3% money growth matching 3% real GDP growth results in 0% inflation with stable velocity, illustrating how money can sustain nominal stability without altering real paths. A misconception is that money growth always leaves prices unchanged due to neutrality, but it can raise or stabilize them depending on real growth. To transfer this, always subtract real output growth from money growth to evaluate effects on nominal variables like inflation.

Based on the money supply growth shown, assume real GDP growth is stable at 0% per year and velocity is stable in the long run. Using quantity theory intuition and the idea that inflation is a monetary phenomenon, which statement best describes the long-run outcome?

Table 6: Money Supply Growth and Inflation (Percent per Year)

Year 1: Money growth 5, Inflation 5

Year 2: Money growth 5, Inflation 5

Year 3: Money growth 5, Inflation 5

Inflation will be about 5% per year because with stable real output, sustained money growth mainly raises the price level in the long run.

The price level will fall because higher money growth reduces the value of money and lowers nominal spending in the long run.

Real GDP will grow about 5% per year because sustained money growth increases long-run productive capacity and employment.

Inflation cannot be predicted because stable velocity implies money growth affects only real variables, not nominal variables, in the long run.

Inflation will be about 0% per year because with stable real output, prices are determined by real factors, not money, in the long run.

Explanation

Monetary growth indicates the annual percentage change in the money supply, and inflation is the rate at which prices generally increase. Long-run money neutrality states that money affects nominal variables like the price level but not real ones like output in the steady state. In this zero real GDP growth setup with 5% money growth and stable velocity, inflation matches at 5%, embodying the monetary theory of inflation where all money growth feeds into prices. A misconception is that stagnant real output means money growth can't cause inflation, yet it does by raising nominal demand without output gains. Practically, compare money growth to real output growth to forecast inflation, revealing how excess money drives price pressures.