Interest Rates and International Capital Flows

Help Questions

AP Macroeconomics › Interest Rates and International Capital Flows

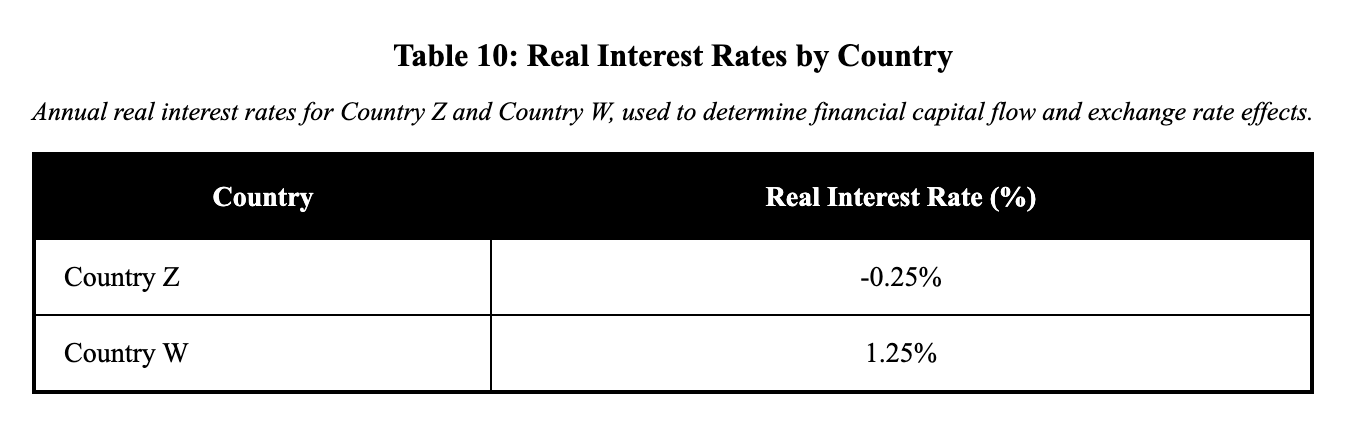

Based on the real interest rates shown in the table, assume both countries’ bonds are risk-free and that the only difference relevant to investors is the real interest rate. Which statement best describes the likely direction of financial capital flows and the exchange-rate effect in the short run?

Table 10. Real Interest Rates (Annual)

- Country Z: $-0.25%$

- Country W: 1.25%

Financial capital will flow toward the country with the higher nominal interest rate, so real rates cannot determine the direction.

Country W’s net exports will rise, so financial capital will flow into Country W and its currency will appreciate.

Financial capital will flow from Country W to Country Z, increasing demand for Country Z’s currency and putting upward pressure on its exchange rate.

Financial capital will flow from Country Z to Country W, increasing demand for Country W’s currency and putting upward pressure on its exchange rate.

Financial capital will not move because real interest rates below zero eliminate international investing incentives.

Explanation

The real interest rate subtracts expected inflation from the nominal rate, illustrating the authentic growth in an investor's real wealth. Higher real rates entice capital inflows from abroad, as they promise superior returns after inflation. In this case, Country W's 1.25% real rate outpaces Country Z's -0.25%, resulting in flows from Z to W and upward pressure on W's exchange rate from increased currency demand. A misconception is that sub-zero rates eliminate all flow incentives, yet investors choose the relatively higher option. Nominal rates can deceive without inflation context. Use the strategy of comparing real interest rates over nominal to predict capital flow patterns and exchange rate pressures effectively.

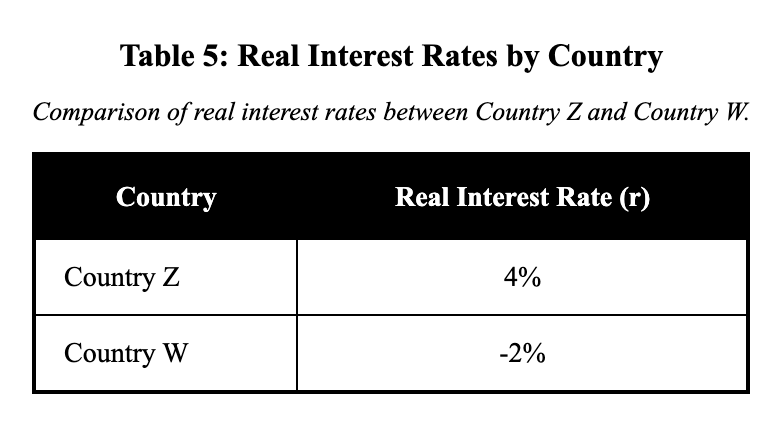

Based on the real interest rates shown in the table (assume equal risk and high capital mobility), which statement best describes capital inflows/outflows and the exchange rate?

Table 5. Real Interest Rates

- Country Z: $r=4%$

- Country W: $r=-2%$

Country Z experiences a financial capital inflow from W, increasing demand for Z’s currency and appreciating it.

No financial capital flows occur because negative real interest rates eliminate international borrowing and lending.

Country Z experiences a trade surplus, so financial capital must flow out of Z and depreciate Z’s currency.

Country Z experiences a financial capital outflow to W, increasing demand for W’s currency and appreciating it.

Capital flows are determined by nominal interest rates, so real interest rates cannot predict inflows or currency movements.

Explanation

The real interest rate, r ≈ i - $π^e$, represents the nominal rate less expected inflation, indicating real investment growth. High capital mobility leads to flows toward superior real returns, influencing exchange rates via currency demand. In Table 5, Country Z's 4% rate far outpaces W's -2%, resulting in inflows to Z from W, appreciating Z's currency. A typical misconception is that negative rates prevent inflows elsewhere, but relative advantages still draw capital. Strategically, focus on comparing real rates, not nominal, to forecast inflows, outflows, and exchange rate movements.

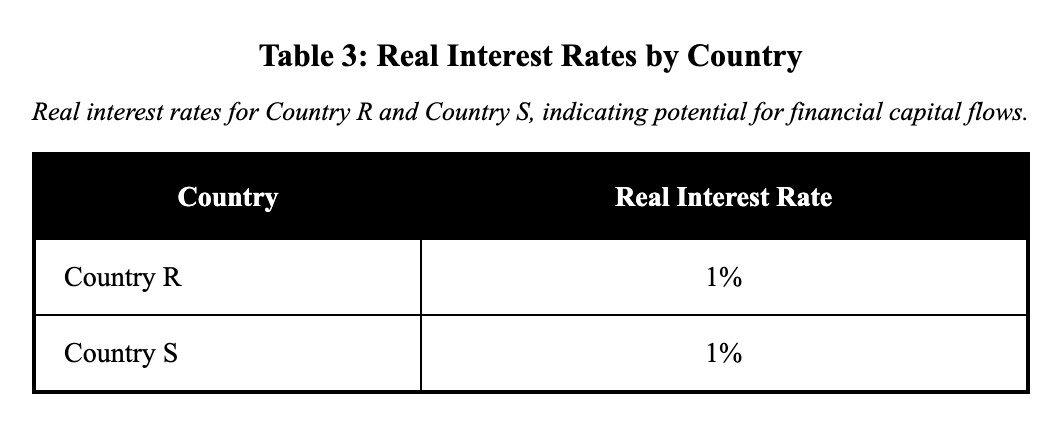

Based on the real interest rates shown in the table (assume equal risk and high capital mobility), which statement best describes financial capital inflows/outflows?

Table 3. Real Interest Rates

- Country R: $r=1%$

- Country S: $r=1%$

Financial capital flows from Country R to Country S, increasing demand for Country S’s currency and appreciating it.

There is no incentive for net financial capital flows between R and S based on real interest rates, so currency demand is unchanged.

Capital cannot move across borders, so real interest rate differences never affect currency demand.

Country R must run a trade deficit, so financial capital flows into Country R and appreciates Country R’s currency.

Financial capital flows from Country S to Country R, increasing demand for Country R’s currency and appreciating it.

Explanation

Real interest rate is the nominal rate minus expected inflation (r ≈ i - $π^e$), providing a measure of real earning power unaffected by price level changes. When real rates are equal across countries, there's no incentive for net capital flows, as returns are comparable assuming similar risks. In Table 3, both Country R and S have 1% real rates, so no systematic capital movement occurs, leaving currency demands stable. A misconception is that trade surpluses or deficits must force capital flows, but equal rates neutralize such pressures from interest differentials. Strategically, compare real interest rates—not nominal—to assess potential for capital flows and exchange rate stability.

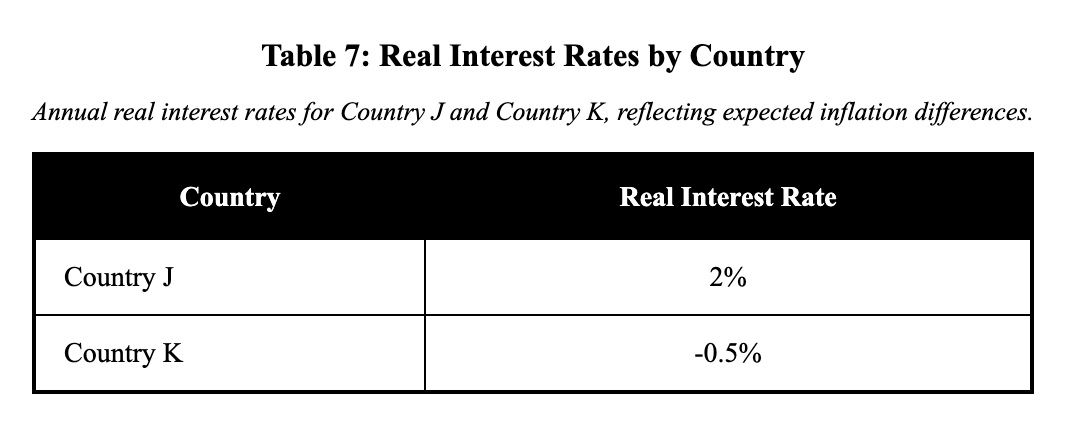

Based on the real interest rates shown in the table, assume expected inflation differs across countries but is already reflected in these real rates. Which option correctly identifies the likely capital flow and its exchange-rate implication in the short run?

Table 7. Real Interest Rates (Annual)

- Country J: 2%

- Country K: $-0.5%$

Country J will have higher imports, so financial capital will flow out of Country J and its currency will appreciate.

Financial capital will not move because negative real interest rates imply investors cannot earn returns abroad.

Financial capital will flow from Country J to Country K, increasing demand for Country J’s currency and putting upward pressure on its exchange rate.

Financial capital will flow from Country K to Country J, increasing demand for Country J’s currency and putting upward pressure on its exchange rate.

Financial capital will flow toward the country with the higher nominal interest rate, so real rates cannot predict the direction.

Explanation

The real interest rate is the nominal interest rate reduced by the anticipated inflation rate, measuring the real profitability of lending or investing. Capital seeks out higher real returns globally to maximize inflation-adjusted gains, influencing currency values through demand shifts. Here, Country J's 2% real rate is higher than Country K's -0.5%, so flows from K to J increase demand for J's currency, exerting upward pressure on its exchange rate. A common misconception is that negative rates make investment impossible, but relative comparisons still guide flows to the least negative option. Confusing nominal with real rates can lead to incorrect predictions, as inflation varies. As a key strategy, compare real interest rates, not nominal, to reliably determine capital flow directions and resulting currency movements.

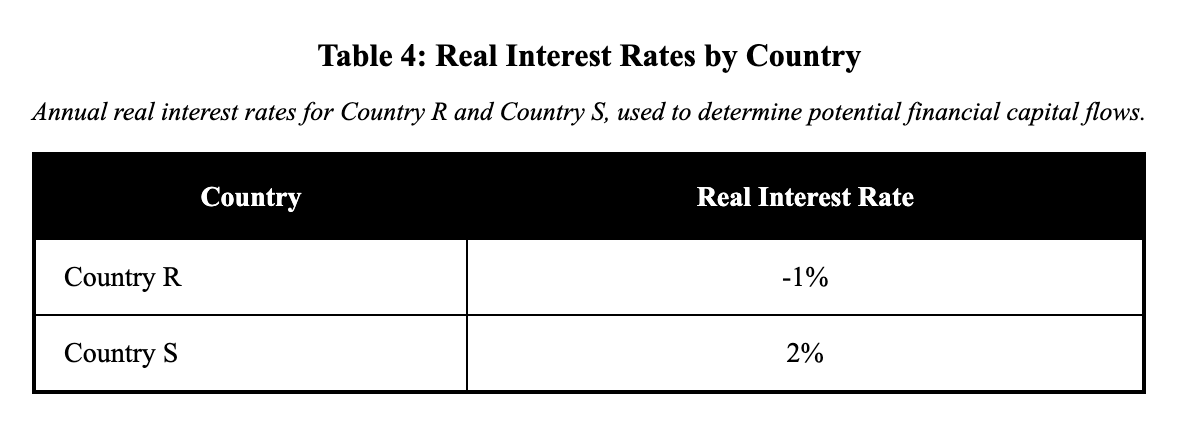

Based on the real interest rates shown in the table, assume investors are choosing between risk-free government bonds in each country and that expected inflation is already incorporated in the real rates. Which outcome is most likely in the short run?

Table 4. Real Interest Rates (Annual)

- Country R: $-1%$

- Country S: 2%

Financial capital will flow from Country S to Country R, increasing demand for Country R’s currency and causing it to appreciate.

Financial capital will not move because negative real interest rates prevent any cross‑border investment.

Financial capital will flow from Country R to Country S, increasing demand for Country S’s currency and causing it to appreciate.

Financial capital will flow toward the country with the higher nominal interest rate, so real rates cannot be used to predict flows.

Country S will import more, so financial capital will flow out of Country S and its currency will appreciate.

Explanation

The real interest rate is the nominal interest rate minus expected inflation, reflecting the genuine return in terms of goods and services an investor can buy in the future. Financial capital moves to countries with higher real rates to secure better real yields, even if rates are negative, as long as they're relatively higher. For these countries, Country S's 2% real rate is preferable to Country R's -1%, prompting flows from R to S and increasing demand for S's currency, leading to its appreciation. A misconception is that negative real rates halt all investment, but investors compare options and may still invest where losses are minimized. It's wrong to assume nominal rates alone dictate flows without inflation adjustments. Remember as a transferable strategy to always evaluate real interest rates, not nominal, when analyzing potential capital flows and exchange rate impacts.

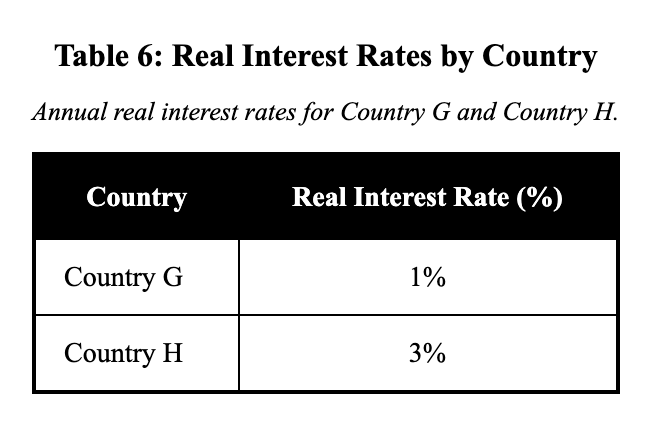

Based on the real interest rates shown in the table, assume the two countries have floating exchange rates and investors seek the highest real return on comparable assets. Which outcome is most likely in the short run?

Table 6. Real Interest Rates (Annual)

- Country G: 1%

- Country H: 3%

Financial capital will not move because real interest rates adjust instantly to eliminate any international differences.

Financial capital will flow toward the country with the higher nominal interest rate, so real interest rates are not relevant.

Financial capital will flow from Country G to Country H, raising demand for Country H’s currency and appreciating it.

Country H’s net exports will rise, so financial capital will flow into Country H and its currency will appreciate.

Financial capital will flow from Country H to Country G, raising demand for Country G’s currency and appreciating it.

Explanation

The real interest rate is derived by subtracting expected inflation from the nominal rate, capturing the actual return on capital in real economic terms. Investors direct financial capital toward higher real rates to achieve greater real wealth accumulation over time. Given Country H's 3% real rate versus Country G's 1%, capital will flow from G to H, elevating demand for H's currency and causing it to appreciate. A frequent misconception is that real rates adjust instantly to equalize, but short-run differences persist and drive flows in open markets. It's also mistaken to assume export increases directly cause capital inflows without interest rates as the catalyst. For transferable insight, always prioritize comparing real interest rates over nominal when assessing international capital dynamics and exchange effects.

Assume two countries have the following real risk-free interest rates: Country J: $r_J=3%$ and Country K: $r_K=7%$. Based on the real interest rates shown, which statement best describes the effect on the foreign exchange market for Country K’s currency in the short run, holding risk constant?

Demand for K’s currency decreases due to capital inflows, putting downward pressure on K’s exchange rate.

Demand for K’s currency is unchanged because financial capital is assumed immobile internationally.

Demand for K’s currency increases because K’s imports rise, putting upward pressure on K’s exchange rate.

Demand for K’s currency increases due to capital inflows, putting upward pressure on K’s exchange rate.

Demand for K’s currency is unchanged because only nominal interest rates affect portfolio flows.

Explanation

Real interest rates guide global capital allocation as investors compare inflation-adjusted returns across countries to maximize purchasing power gains. Country K's 7% real return substantially exceeds Country J's 3%, making K the preferred destination for international investment capital. When foreign investors buy K's bonds or assets, they must first purchase K's currency, increasing its demand in foreign exchange markets. This surge in demand for K's currency puts upward pressure on its exchange rate, causing K's currency to appreciate relative to J's. A common error is thinking capital inflows weaken currencies or that only trade affects exchange rates, but capital flows are major currency demand drivers. Remember: higher real rates attract capital inflows, which require currency purchases that strengthen the recipient's exchange rate.

Country S reports a nominal interest rate of $i_S=6%$ and inflation of $\pi_S=4%$, while Country T reports a nominal interest rate of $i_T=5%$ and inflation of $\pi_T=1%$. Using $r\approx i-\pi$, the real rates are $r_S\approx2%$ and $r_T\approx4%$. Based on the real interest rates shown, which financial capital flow is most likely in the short run, holding risk constant?

Financial capital flows from Country S to Country T, creating net capital inflow to T and net capital outflow from S.

Financial capital remains in Country S because its nominal interest rate is higher than Country T’s.

No capital flows occur because converting nominal to real eliminates interest-rate incentives.

Financial capital flows from Country T to Country S, creating net capital inflow to S and net capital outflow from T.

Country S runs a trade deficit, so financial capital must flow from S to T to finance imports.

Explanation

Real interest rates equal nominal rates minus inflation, revealing true investment returns after accounting for price level changes. Country S offers 2% real return (6% - 4%), while Country T provides 4% real return (5% - 1%), making T more attractive despite its lower nominal rate. Rational investors will shift capital from S to T to capture the higher real return, creating net capital outflow from S and net capital inflow to T. Many students mistakenly focus on nominal rates or assume higher inflation countries attract capital, but only real returns matter for investment decisions. The crucial lesson: always convert nominal to real rates using r ≈ i - π, then identify capital flow direction toward the higher real rate.

Based on the real interest rates shown (assume equal risk and high capital mobility), which outcome is most likely in the short run?

Real interest rates (annual): Country A: 4%, Country B: 1%

Financial capital will flow from Country B to Country A, increasing demand for Country A’s currency and putting upward pressure on its exchange rate.

Country A will run a trade surplus, so financial capital will flow into Country A and its currency will appreciate.

Financial capital will flow from Country A to Country B, increasing demand for Country B’s currency and putting upward pressure on its exchange rate.

Because the real interest rate does not affect financial returns, there will be no significant international capital flows between the countries.

Financial capital will flow toward the country with the higher nominal interest rate, even if its real interest rate is lower, causing its currency to appreciate.

Explanation

The real interest rate represents the actual return on investment after adjusting for inflation, making it the key factor in international capital flow decisions. When Country A offers a 4% real return while Country B offers only 1%, rational investors will move their financial capital from Country B to Country A to earn the higher return. This capital flow increases demand for Country A's currency as investors need to convert their money to invest there, putting upward pressure on Country A's exchange rate. A common misconception is that nominal interest rates drive capital flows, but investors care about real purchasing power gains. The strategy is simple: compare real interest rates between countries—capital flows toward the higher real rate, strengthening that country's currency.

Based on the real interest rates shown (assume equal risk and high capital mobility), which statement best describes the direction of financial capital flows?

Real interest rates (annual): Country X: 0%, Country Y: 3%

Country Y’s exports will rise, so financial capital will flow into Country Y and its currency will appreciate.

Financial capital will not move because investors respond only to nominal interest rates, not real interest rates.

Financial capital will flow from Country Y to Country X, raising demand for Country X’s currency and tending to appreciate it.

Financial capital will flow from Country X to Country Y, raising demand for Country Y’s currency and tending to appreciate it.

Financial capital will remain unchanged because international capital is immobile in the short run even with interest rate differences.

Explanation

Real interest rates measure the true return on investment by removing the effects of inflation, allowing meaningful comparison across countries. Country Y's 3% real rate offers a better return than Country X's 0% real rate, so investors will move financial capital from Country X to Country Y to maximize their returns. This movement requires converting Country X's currency into Country Y's currency, increasing demand for Country Y's currency and tending to appreciate it. Many students mistakenly think only nominal rates matter or that capital is immobile, but in reality, financial capital moves quickly toward higher real returns. To analyze capital flows, always compare real interest rates—the country with the higher real rate attracts capital inflows and experiences currency appreciation pressure.