Perfectly Competitive Output Markets

Help Questions

AP Microeconomics › Perfectly Competitive Output Markets

If the United States trades computers in exchange for cars from Germany, what must be true?

The United States has comparative advantage in producing computers and Germany has comparative advantage in producing cars

The United States has comparative advantage in producing cars and Germany has comparative advantage in producing computers

The United States has absolute advantage in producing computers and Germany has comparative absolute in producing cars

The United States has absolute advantage in producing cars and Germany has absolute advantage in producing computers

None of the other answers

Explanation

Comparative advantage refers to the ability of a party to produce a particular good at a lower opportunity cost than another party. When trading, countries will always gain by trading the good in which they have comparative advantage in producing. Since the US is trading computers for cars from Germany, the US must have comparative advantage in computer production while Germany has comparative advantage in car production.

The following question is based on this table:

What is the marginal cost of producing the fourth good?

Explanation

Marginal cost is the increase in the total cost of production to produce one additional unit. In this case, we want to determine the marginal cost of producing the fourth good. The total cost for producing three goods is 26 and the total cost for producing four goods is 29. Because total cost increases by 3, 3 is the fourth good's marginal cost.

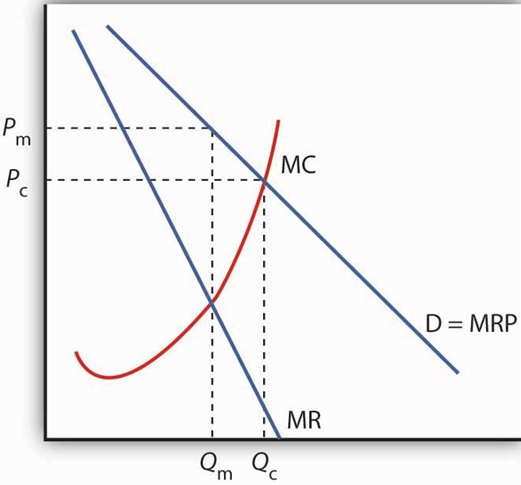

Compared to a perfectly competitive market, a monopolist produces...

less of a good and charges a higher price.

less of a good and charges a lower price.

more of a good and charges a higher price.

more of a good and charges a lower price.

Unable to determine from the information given.

Explanation

As seen in the graph below, the monopolist faces a downward sloping marginal revenue curve that is steeper than the demand curve. The monopolist produces where MC = MR which results in a higher price and lower output compared to where the marginal cost curve meets the demand curve, which is where equilibrium would be in a perfectly competitive market.

Use the following table to answer the question below:

| Units | Total Variable Cost | Price |

|---|---|---|

| 1 | 10 | 20 |

| 2 | 18 | 19 |

| 3 | 24 | 18 |

| 4 | 28 | 17 |

| 5 | 30 | 16 |

| 6 | 33 | 15 |

| 7 | 38 | 14 |

| 8 | 44 | 13 |

| 9 | 52 | 12 |

| 10 | 61 | 11 |

Above is a portion of the cost structure for a theoretical firm with total fixed costs of 30. Which of the following can you say about this portion of the firm's cost structure?

Increasing returns to scale

Decreasing returns to scale

Constant returns to scale

None of the other answers

Explanation

The firm's average total costs are decreasing throughout this range. Therefore, there are increasing returns to scale within this range.

| Units | Total Variable Cost | Total Cost | Avg. Cost |

|---|---|---|---|

| 1 | 10 | 40 | 40 |

| 2 | 18 | 48 | 24 |

| 3 | 24 | 54 | 18 |

| 4 | 28 | 58 | 14.5 |

| 5 | 30 | 60 | 12 |

| 6 | 33 | 63 | 10.5 |

| 7 | 38 | 68 | 9.7 |

| 8 | 44 | 74 | 9.25 |

| 9 | 52 | 82 | 9.11 |

| 10 | 61 | 91 | 9.1 |

An oligopolistic industry would most likely have

substantial barriers to entry

no barriers to entry

a large number of firms

one firm with no close rivals

price-taking behavior

Explanation

An oligopolistic industry is dominated by a small number of firms. Oligopolies are typically caused by significant barriers to entry, which enable a few firms to dominate the industry.

If an increase in the price of pizza causes a decrease in the demand for soda, then the two goods are:

complementary goods

substitute goods

normal goods

luxury goods

giffen goods

Explanation

If an increase in the price of pizza causes a decrease in the demand for soda, then the two goods are complementary goods, or goods that are typically consumed together. Thus, the two goods' demand are affected by the demand of the other good. As the price of pizza increases, its demand will likely decrease. The decrease in demand for pizza causes a decrease in demand for soda because the two goods are complementary.

Use the following table to answer the question below:

| Units | Total Variable Cost | Price |

|---|---|---|

| 1 | 10 | 20 |

| 2 | 18 | 19 |

| 3 | 24 | 18 |

| 4 | 28 | 17 |

| 5 | 30 | 16 |

| 6 | 33 | 15 |

| 7 | 38 | 14 |

| 8 | 44 | 13 |

| 9 | 52 | 12 |

| 10 | 61 | 11 |

Consider the above cost and price schedule for a theoretical firm. Assume the firm has fixed costs of 30. Within the range shown in the table, at what point are the firm's average costs lowest?

Explanation

| Units | Total Variable Cost | Total Cost | Avg. Cost | Price |

|---|---|---|---|---|

| 1 | 10 | 40 | 40 | 20 |

| 2 | 18 | 48 | 24 | 19 |

| 3 | 24 | 54 | 18 | 18 |

| 4 | 28 | 58 | 14.5 | 17 |

| 5 | 30 | 60 | 12 | 16 |

| 6 | 33 | 63 | 10.5 | 15 |

| 7 | 38 | 68 | 9.7 | 14 |

| 8 | 44 | 74 | 9.25 | 13 |

| 9 | 52 | 82 | 9.11 | 12 |

| 10 | 61 | 91 | 9.1 | 11 |

The following question is based on this table:

What production level maximizes the firm's profits?

Impossible to determine from the given information.

Explanation

The profit maximizing quantity for the production of goods is the level at which marginal cost equals marginal revenue. This table allows us to easily determine the marginal cost of producing the _n_th good, but it does not give any information about the marginal revenue associated with selling th _n_th good (i.e. market price of the good).

Energy can be generated using either coal or natural gas as an input. If the supply of coal is interrupted, what are the most likely effects on the price and quantity of natural gas traded on the open market? Assume a perfectly competitive market with no government policy intervention.

Price increases, Quantity increases

Price decreases, Quantity increases

Price decreases, Quantity decreases

Price increases, Quantity decreases

No change

Explanation

Coal and natural gas are substitutes for each other based on the description given in the question. Therefore, an interruption in the supply of coal will lead to an increase in the demand for natural gas. This will increase both the price and quantity of natural gas.

The law of diminishing marginal utility explains:

the diminishing marginal product of capital

law of demand

law of supply

law of comparative advantage

law of inequality

Explanation

The law of diminishing marginal utility states that the marginal value derived from a unit decreases as its use increases. This explains the phenomenon where the use of capital (its marginal product) decreases or diminishes as its utilization increases.